All AstroNova Stakeholders Invited to Meet and Interact with Askeladden’s Board Candidates

Askeladden Nominees Have Specific and Relevant Expertise to Execute Askeladden’s Plan to Maximize Value

Transdigm’s Recently Raised Bid for Aerospace Components Company Servotronics Highlights Potential to Unlock Value at AstroNova with Better Governance

FORT WORTH, TX / ACCESS Newswire / June 2, 2025 / Dear AstroNova stakeholders:

I write to you as the founder and portfolio manager of Askeladden Capital (collectively, “we,”) which is AstroNova’s largest shareholder, owning approximately 9.2% of the company on behalf of our clients.

In an effort to improve AstroNova’s performance for the benefit of shareholders, employees, and all other stakeholders, we have nominated five highly qualified individuals for election to AstroNova’s Board of Directors at the company’s Annual Meeting, scheduled for July 9, 2025.

We invite you to join an Investor Forum where shareholders, employees, and all other interested parties can interact directly with our nominees. After a brief introduction and panel discussion of approximately 20 minutes, we will open up the call for Q&A.

We will conduct this “town hall” style meeting virtually via Zoom at 11:00 AM Eastern Time (10:00 AM Central Time) on Thursday, June 12, 2025. You can register here :

https://zoom.us/webinar/register/WN_P4nfq0iOSamSBEiaDZ0IZA#/registration

Please contact Samir Patel via samir@askeladdencapital.com if you have any trouble registering.

Attendees will have the option to remain anonymous to all parties other than the host. Those who cannot attend live are also invited to email us with written questions that we will read and answer during the town hall as time permits. A recording of the call will subsequently be made available.

We encourage candid and detailed questions – the more challenging the better – about our research, our plan, our nominees’ backgrounds, and how we will work as a team to maximize the value of AstroNova for all. Please ask similar questions of the incumbents, then vote based on whose answers you find more compelling.

Askeladden has researched AstroNova since 2016 and been a 5% shareholder since 2020. Since March, we have spoken to over 15 individuals, ranging from former employees to suppliers and other industry veterans, to deepen our understanding of the company. In the near future, we will share selected research findings with AstroNova shareholders.

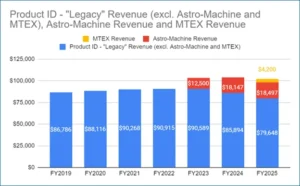

We believe AstroNova has many strengths, such as a large installed base and many talented employees. Unfortunately, we believe that these attractive qualities have been overwhelmed by poor governance and management by the incumbent Board, and CEO Greg Woods, which has harmed shareholders and employees alike. In FY2025, the company reported Adjusted EBITDA of $12.3 million, substantially below FY2024’s $17.6 million and FY2025 original guidance of ~$21 million at the midpoint. [1]

The company’s May 2024 acquisition of MTEX should have further enhanced profitability – instead, the CEO and Board’s decision to spend $18.7 million in cash and assume additional debt [2] to fund this acquisition harmed both shareholders and employees. The share price fell almost 50% over the ensuing year, [3] while employees have faced layoffs. [4]

In FY2025, MTEX generated an operating loss of $16.9 million, including a goodwill impairment of $13.4 million, and the company subsequently discontinued 70% of MTEX’s product portfolio. [5] [6]

As a result of the lower earnings and increased debt due to the MTEX acquisition, the company breached its debt covenants and suffered an event of default under its credit facility during the quarter ended January 31, 2025 (thus forcing AstroNova to seek a waiver from its lender, which was subsequently granted). [7]

While CEO Greg Woods retains his job despite this self-inflicted debacle, many AstroNova employees were not so lucky: on March 20, 2025, the company announced “the reduction of approximately 10% of the Company’s global workforce, primarily in the PI [Product Identification] segment.” [8] Through no fault of their own, rather than enjoying the profit-sharing and career growth opportunities that a well-managed company should provide, 10% of AstroNova employees lost their jobs.

Despite these missteps, incumbents appear to be doubling down on this failed strategy, and have refused to engage with Askeladden’s efforts to improve the company’s performance.

We recently published a 20-page document including our specific, research-based plan for improving AstroNova’s performance, as well as relevant background information on the company’s performance and governance. We believe that our nominees have specific and relevant qualifications to address the current challenges faced by AstroNova. Below is their biographical information.

Shawn Kravetz. Mr. Kravetz has relevant experience as a change agent under similar circumstances. He joined the Board of Nevada Gold & Casinos, Inc. as a large shareholder frustrated by performance, including a recent acquisition. He served from 2016 until Nevada Gold was sold in 2019, including Chairman of the Corporate Governance and Nominating Committee. Mr. Kravetz was recently nominated for election to the Board of publicly traded Spruce Power Holding Corporation by the company’s Nominating and Governance Committee. [9]

Jeff Sands. As Mr. Sands discusses in his book, “Corporate Turnaround Artistry: Fix Any Business in 100 Days,” he has successfully used techniques included in our plan to restore profitability at numerous businesses, including some merely weeks away from lender-forced liquidation. He has won the Turnaround Management Association “Turnaround of the Year” award three times. Mr. Sands has successfully worked with businesses such as a $100M supplier of aerospace components to Boeing (~2x the size of AstroNova’s Aerospace segment), as well as complex and capital-intensive businesses such as steel and pharmaceuticals. Given AstroNova’s significant recent decline in profitability and elevated inventory balances, Mr. Sands’ experience in driving rapid cash flow improvement is extremely relevant. Mr. Sands has been involved in the sale of numerous private companies.

Ryan Oviatt. Mr. Oviatt has extensive experience – as CFO, CEO, and Board Member of Profire – of managing an industrial products business for margin and cash flow in the highly cyclical energy market. Mr. Oviatt managed a team that used techniques such as automation of manual processes and key administrative functions, customer outreach, and performance-based incentive compensation programs designed to instill a sense of ownership throughout the company. Mr. Oviatt helped lead the successful sale of Profire to a strategic public-company buyer, CECO Environmental. After multiple rounds of negotiation, Profire successfully achieved a final offer price 27.5% higher than CECO’s original offer, and an all-cash deal rather than the original offer of 75% cash and 25% stock. This final offer represented a 60.3% premium to Profire’s volume-weighted average share price over the 30 days prior to the Board approving the merger. [10]

Boyd Roberts. Mr. Roberts was the youngest member of the executive team at Franklin Covey (FC) and has integrated and substantially grown an acquired division, with ownership of full P&Ls and high employee net promoter scores. Mr. Roberts has extensive experience with Franklin Covey’s customer-focused recurring-revenue business model. Mr. Roberts is fluent in Portuguese. His linguistic and cultural strengths uniquely qualify him to address the challenging MTEX acquisition, which we believe has suffered due to a cultural mismatch between the labor force at its facility in Porto in northern Portugal, and AstroNova’s American business culture. [11]

Samir Patel. As AstroNova’s largest shareholder, who has researched the business since 2016, I am deeply familiar with the company’s ongoing (flawed) strategy, contrary to the company’s misleading assertion that the company will be damaged by a new Board “unacquainted with recent decision-making .” [12] I will ensure that AstroNova’s operational and capital allocation decisions consistently maximize shareholder value.

As a point of comparison on what AstroNova could potentially be worth with better governance, we note that Servotronics (SVT), a global designer and manufacturer of servo controls and other components for aerospace and defense applications, announced a merger with large aerospace manufacturer Transdigm (TDG) for $110 million in cash on May 19, 2025, and subsequently raised the offer price by ~22% from $38.50 to $47.00 after Servotronics received another offer from a competing bidder, suggesting significant interest in the business at that valuation. [13] Even the original offer price – let alone the subsequent increase – is almost identical to AstroNova’s entire enterprise value as of May 20, 2025. [14] [15]At the original offer price, the all-cash transaction represented a 274% premium to Servotronics’ share price at the prior close. For the fiscal year 2024, Servotronics generated $44.9 million in revenue with only $8.2 million in gross profit and less than $1 million in Adjusted EBITDA. [16]

Meanwhile, for its FY2025 which ended a month later, AstroNova’s Test and Measurement segment (subsequently renamed Aerospace) generated a slightly higher $48.9 million in revenues with a much higher $11.1 million in segment operating profit. It seems reasonable to assume that a buyer evaluating these two businesses side by side would assign a higher valuation to AstroNova Aerospace given its modestly higher revenues and substantially higher profits. In other words (and apart from any tax considerations), that would imply that if AstroNova Aerospace was sold at a similar value to Servotronics’ original agreement – let alone the higher subsequent agreement raising the offer amount by over 20% – AstroNova could pay off all its debt and return cash to shareholders equivalent to roughly the current share price. Shareholders would then still own the entire Product Identification segment, with slightly over $100 million in annual revenues generated each of the past three fiscal years, which is clearly worth substantially more than the zero or even negative value implied if Servotronics’ valuation is applied to AstroNova Aerospace. [17]

While the Servotronics transaction is merely one data point, it demonstrates the potential value if AstroNova implements the strategy we have developed – which we recently presented in our public plan – rather than doubling down on a strategy promoted by the value-destroying incumbent CEO and Board. In the more than eleven years from February 1, 2014 (when Mr. Woods became CEO) through May 15, 2025 (the record date of this year’s Annual Meeting), AstroNova shares have experienced a total return of negative 28%. [18]

You can find further information about the upcoming board election, scheduled for July 9, 2025, at the AstroNova page on the Askeladden Capital website : https://www.askeladdencapital.com/astronova/

These documents will also be available at no cost at www.sec.gov .

As stated previously, the “town hall” will occur virtually via Zoom at 11:00 AM Eastern Time (10:00 AM Central Time) on Thursday, June 12, 2025. You can register here :

https://zoom.us/webinar/register/WN_P4nfq0iOSamSBEiaDZ0IZA#/registration

Please feel free to reach out to me with any questions or comments, at samir@askeladdencapital.com or (682) 553-8302. We look forward to earning your vote.

Cordially,

Samir Patel

Founder and Portfolio Manager, Askeladden Capital

Samir Patel, Askeladden Capital Management LLC, Jeff Sands, Shawn Kravetz, Ryan Oviatt and Boyd Roberts (collectively the “Participants”) filed a definitive proxy statement and accompanying proxy card with the SEC on May 20, 2025, as amended on May 21, 2025, to be used in soliciting proxies in connection with the 2025 annual meeting of shareholders (the “Annual Meeting”) of AstroNova, Inc. (the “Company”). All shareholders of the Company are advised to read the Proxy Statement and other documents related to the solicitation of proxies, each in connection with the Annual Meeting, by the Participants, as they contain important information, including additional information related to the Participants, including a description of their direct or indirect interests by security holdings or otherwise. The Proxy Statement and an accompanying GOLD proxy card will be furnished to some or all of the Company’s stockholders and is, along with other relevant documents, available at no charge on the SEC website at http://www.sec.gov, or by contacting Samir Patel at 1452 Hughes Road, Suite 200 #582, Grapevine, TX, 76051.

[1] Q4 FY2024 and Q4 FY2025 Earnings Release.

[2] FY2025 Form 10-K filed April 15, 2025.

[3] Stock price data from YCharts.

[4] FY2025 Form 10-K, page 24.

[5] AstroNova Form 10-K for FY2025. Impairment discussed on page 11; purchase price discussed on page 15.

[6] MTEX Acquisition Announcement and Conference Call Transcript (May 9, 2024) and FY2025 Form 10-K filed April 15, 2025.

[7] Form 8-K Earnings filed March 21, 2025.

[8] FY2025 Form 10-K, page 24.

[9] Spruce Power Holding Corp Definitive Proxy, page 10.

[10] Profire Energy (PFIE) SC14D9 dated December 3, 2024. Section “Background of the Offer and the Merger” on pages 9 – 16. https://www.sec.gov/Archives/edgar/data/1289636/000110465924124898/tm2429518-1_sc14d9.htm

[11] “The American work culture focuses on ambition… in Portugal, there is a more collective approach to work and less pressure… [people] tend to place greater importance on personal well-being, family time, and life outside of work.” LXUS (Corporate Relocation service provider.) https://www.lxusportugal.com/blog-lxusportugal/cultural-comparison-between-the-usa-and-portugal

[12] Letter accompanying AstroNova’s definitive proxy statement, filed May 19, 2025.

[13] “TransDigm raises offer price for Servotronics to $47/share.” Seeking Alpha. May 29, 2025. https://seekingalpha.com/news/4453416-transdigm-raises-offer-price-for-servotronics-to-47-share

[14] “Transdigm to Acquire Servotronics For About $110 million.” Nasdaq. May 19, 2025. https://www.nasdaq.com/articles/transdigm-acquire-servotronics-about-110-mln

[15] Per data sources such as Seeking Alpha, ALOT shares closed at $9.12 on May 20, 2025. The company’s recent definitive proxy statement, filed May 19, 2025, discloses a recent sharecount of approximately 7.6 million shares, for a market cap of approximately $69 million as of that date. AstroNova’s Form 10-K filed April 15, 2025 discloses $20.9 million outstanding on the revolving credit facility, $6.1 million in current long-term debt, $0.6 million in short-term debt, and $19 million in long-term debt, for a total of $46.6 million in gross debt. The same Form 10-K disclosed $5 million of cash and equivalents, making net debt $41.6 million. The sum of $41 million and $69 million is approximately $110 million.

[16] Form 10-K for Servotronics SVT filed March 17, 2025.

[17] AstroNova Form 10-K for FY2025, filed April 15, 2025. Page 24.

[18] Data from YChart

Samir Patel

samir@askeladdencapital.com

(682) 553-8302

SOURCE: Askeladden Capital Management LLC

View the original press release on ACCESS Newswire